Despite the major changes to the Federal Budget that have gone by since President Trump took office, I'm getting the feeling that it's all just "the same old bullshit" we've been going through for decades. Yes, I'm reading of government shutdowns coming. As usual, it's going to shutdown "if they can't agree to a budget." Ars Technica (who are apparently 100% in the crowd that says, "yes cut the budget, but don't you DARE cut what I want!) summarized it this way: "In a win for science, NASA told to use House budget as shutdown looms."

The White House proposed a budget earlier this year with significant cuts for a number of agencies, including NASA. In the months since then, through the appropriations process, both the House and Senate have proposed their own budget templates. However, Congress has not passed a final budget, and the new fiscal year begins on October 1.

As a result of political wrangling over whether to pass a "continuing resolution" to fund the government before a final budget is passed, a government shutdown appears to be increasingly likely.

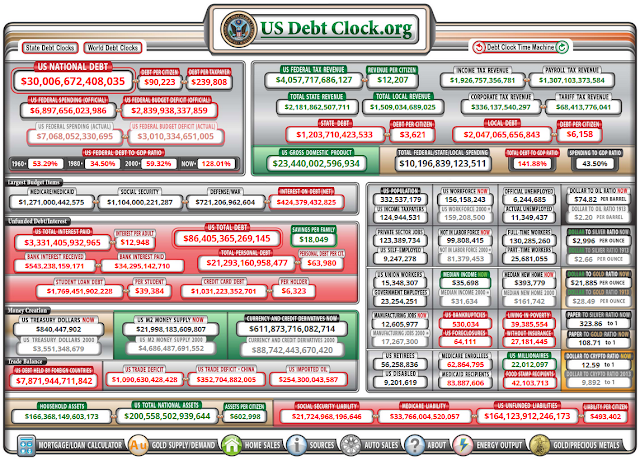

While we haven't had an actual government shutdown in a few years, it's just the same old routine used all the time. As for passing a budget, one of the actual duties assigned to the legislative branch, it still seems to be that the most recent Federal budget to be passed and signed was in 1997. That's actually a polite and kind way of summing up the situation. I say it's kind because it implies that congress has only been so bad in doing their jobs since 1997. A better picture is conveyed by a quote attributed to South Carolina's Nikki Haley (governor at the time), "in the past 40 years, Congress has passed a pathetic four budgets on time."

What they do that allows them to keep spending at nearly infinite levels is to pass those "continuing resolutions" mentioned in the first quote to legalize the spending.

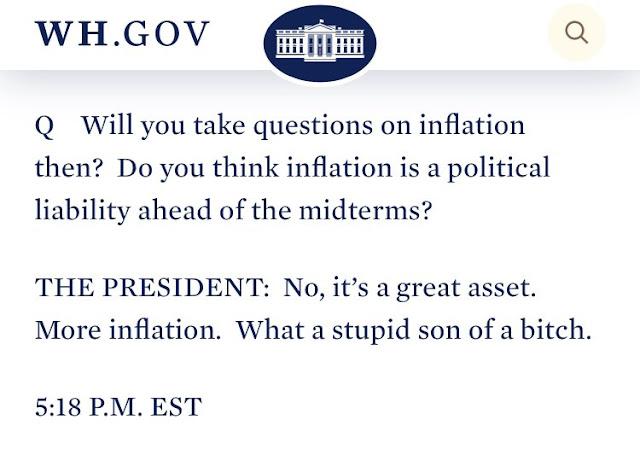

My guess is that if the media wasn't so tied up with the story about Charlie Kirk, they'd be blabbering about a looming government shut down, with the usual Gloom and Doom talk.

Things like this recurring story are one of the reasons I've drastically cut back on the amount of politics and economics writing I used to do. I'm so bored with writing about this, I'll just get to the essence of why I'm here. If you want the long story, go to this 2023 post.

So why do we go through this crap every time the subject comes up?

Political theater. Kabuki (overly dramatic) theater. They drag it

out to the last minute so they can look like heroes. If they shut down

the Fed.gov, so what? Those workers get their time off and their pay, so

it's "no harm? no foul." Feel sorry for them? I think if one works

for fed.gov, one should have a savings buffer of a few weeks to ensure you can

buy your groceries in the event of a shutdown. It's not like nobody

knows a shutdown is coming.

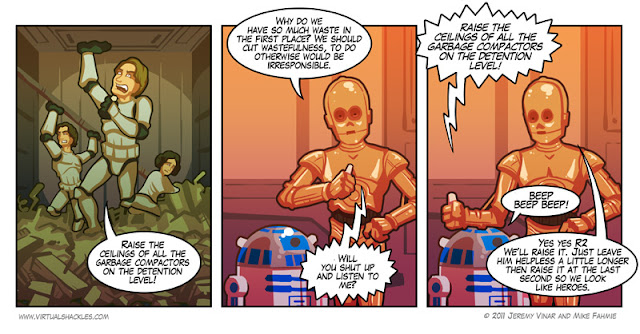

There's a cartoon I've been running for years, almost every reference to the

debt ceiling since 2013, that I really think sums up the whole story. In

a way, a Star Wars parody reference.

Yup. They drag it out as long as they want, make it sound as dire as possible, all so that they can look like heroes, as in the last panel. I went to the website referred to in the lower left of the cartoon and the web site appears to be gone, with a Vietnamese language site there.